After Trump's Speech, BTC Breaks Below 67K — The Five-Condition Structure Behind Oil, Rates, Whale Capitulation, and Ripple Prime

Bitcoin fell below 67K after Trump's national address. Hormuz blockade with $150 oil warnings, rising rate hike probability, whale capitulation, demand absence, and Ripple Prime's BBB rating — a deep-dive into the five structural conditions the video couldn't fully unpack.

Why the market abandoned its ceasefire hopes, and where Bitcoin might find room to breathe

DATA BOX

Market Environment BTC price: $66,470 (down 2.85% daily) | Brent crude: ~$110/barrel | Dollar index: 100+ | Fear & Greed index: 8 (extreme fear)

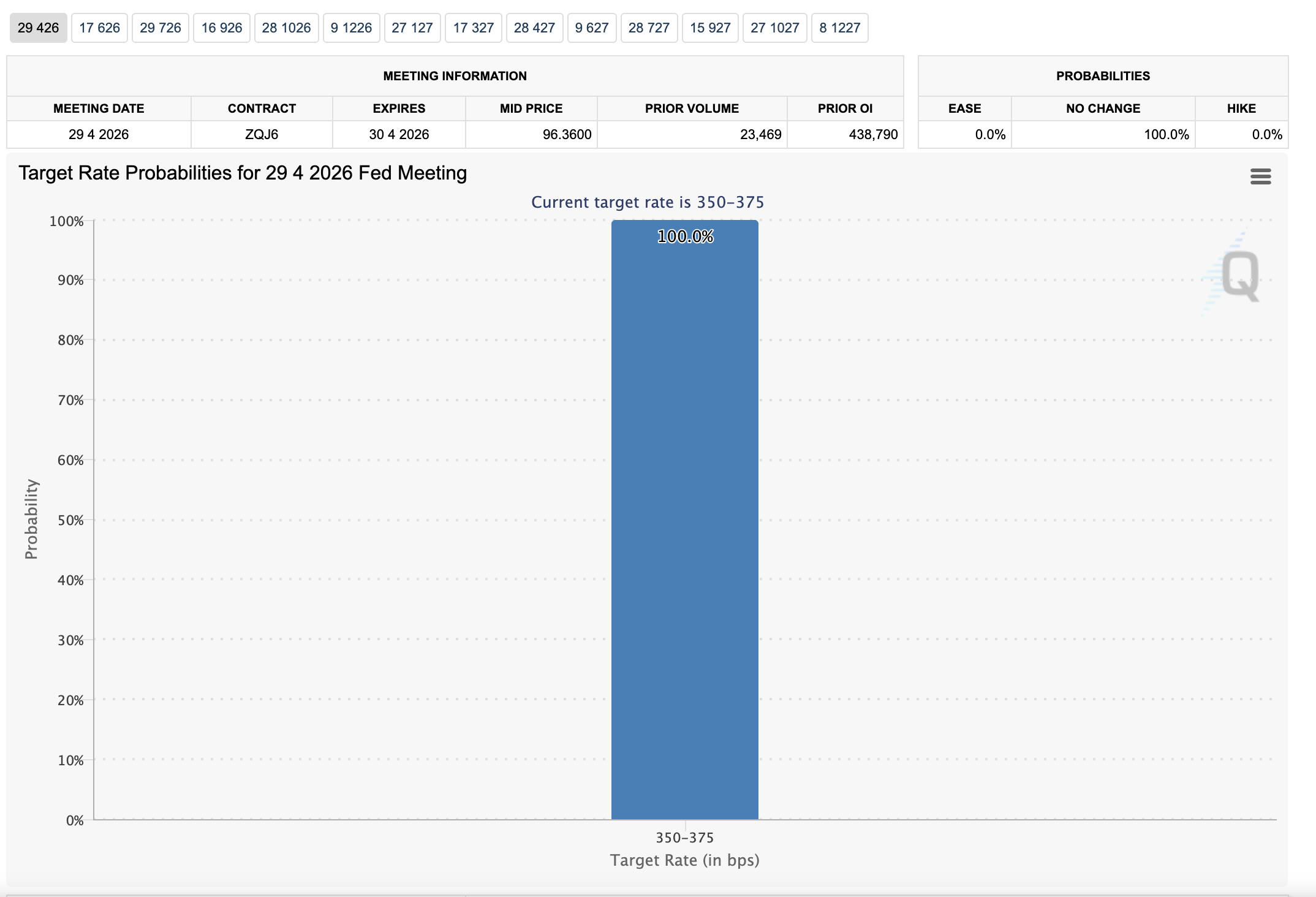

Macro Variables April FOMC hold probability: 99.5% | June 25bp cut probability: 6% | December rate hike probability rising to ~25% | JP Morgan: oil could hit $150 if Hormuz blockade extends one more month

BTC Internal Supply/Demand Whale address net realized P&L 7-day EMA: daily losses exceeding $200M | Apparent demand: -63,000 BTC (end of March) | March ETF net inflows: $1.13B → final week flipped to -$296M

Ripple Prime KBRA BBB rating assigned (Apr 2, 2026) | Hidden Road acquisition: $1.25B | Annual clearing: $3T+ | Institutional clients: 300+ | Additional 2026 capital injection: ~$500M expected

In the video, the analysis covered five issues in sequence to explain why the market flipped back to risk-off after Trump's address to the nation. The goal was to walk through the chain — oil → rates → selling pressure → rebound conditions → Ripple Prime — in a single sitting, which meant certain links between data points and their deeper context could not be fully explored. This post fills those gaps. Where the video focused on "what is happening," this text focuses on "why it is happening, and how each condition reinforces or offsets the others."

The current market picture is not simple. Bitcoin is trading around $66,470 according to Yahoo Finance data, and BeInCrypto's Fear & Greed index sits at 8 — deep in extreme fear territory. Brent crude is hovering near $110 per barrel. The dollar index has climbed above 100. These figures describe not a crypto-specific selloff but a classic risk-aversion regime in which dollar strength and surging energy prices are compressing risk assets simultaneously.

The central argument of this post is straightforward. Bitcoin's break below 67K was not caused by a single event. It was the product of five structural conditions firing at the same time. And any recovery will not be triggered by a single piece of good news either — it will require at least three of those five conditions to ease simultaneously. Here is what each one looks like on the inside.

1. The Strait of Hormuz: How Oil Prices Weigh on the Entire Market

In the video, the causal chain — "Hormuz blockade persists → oil rises → Bitcoin gets pressured" — was covered at speed. Here, each link in that chain is examined more precisely.

Trump's April 1 address did not deliver what the market was hoping for. Synthesizing the available reporting, the key takeaways were: a promise of intensified strikes over the coming two to three weeks, a signal that the U.S. would step back from protecting the Strait of Hormuz and leave that responsibility to other nations, and the absence of any concrete roadmap for ending the war or reopening the strait. The New York Times assessed the speech as containing nothing new — essentially a recitation of the same points Trump had been posting on social media for the past month. For the market, this was not relief. It was a prompt to reprice risk upward.

The real-world impact on the Strait of Hormuz is quantifiable. According to Korea Maritime & Ocean Corporation analysis, traffic through the strait has dropped roughly 80% from normal levels, and VLCC (very large crude carrier) freight rates on the Middle East–China route have tripled in one month. Approximately one-fifth of the world's oil and LNG transits this narrow waterway. When a bottleneck of this magnitude persists not for days but for weeks, it stops being a Middle East headline and becomes a global inflation story.

JP Morgan chief economist Bruce Kasman warned that if the Hormuz blockade extends by another month, Brent crude could reach $150 per barrel. Goldman Sachs similarly left the door open to $150 if oil flows are not normalized within the month. What matters here is not the $150 figure in isolation but the growing market consensus that elevated oil prices could be structural rather than temporary.

The transmission mechanism from high oil to Bitcoin deserves a more granular breakdown than the video provided. The pathway involves several intermediate steps.

First, an oil price surge directly pushes up the energy component of the Consumer Price Index. Energy carries roughly a 7% weight in U.S. CPI, but its pass-through effects — on transportation costs, manufacturing input prices, and food — are significantly larger than the headline weight suggests.

Second, when inflation concerns resurface, the Fed loses room to cut rates. Deferred rate cuts push bond yields higher, which in turn strengthens the dollar.

Third, a stronger dollar creates dual pressure on Bitcoin: the asset's relative attractiveness declines, and the currency conversion effect works against non-dollar holders.

Reading Bitcoin's short-term movements through charts alone therefore misses the point. The chart has oil and the dollar layered on top of it. The question the market is asking right now is not "is there a war?" but "how long does the war remain a pricing variable?" If geopolitical tension escalates for a day or two, markets adapt. But when a core supply-chain risk like Hormuz stays alive on a weekly or monthly basis, oil, consumer spending, corporate costs, inflation, and rate expectations all move together.

2. The Fed: From "Rate Cut Delay" to "Rate Hike Possibility"

The CME FedWatch numbers — 100% probability of a hold in April, 6% probability of a June cut — were delivered quickly with the conclusion that "cut expectations are being pushed back." In text, there is room to explain why this shift represents a qualitative change in market psychology, not just a numerical adjustment.

As recently as mid-March, some residual hope for a June cut was still alive in the futures market. But as the war and oil shock continued, the rate futures market began pushing the expected timing of the first cut toward September. A Reuters poll of economists confirmed this view: the consensus was that the Fed would hold rates steady through at least September.

Then, around March 20, a qualitative shift occurred. CME FedWatch began reflecting approximately 25% probability of a rate hike by December. Just days earlier, the probability of any hike had been virtually zero. This is not a routine numerical move. It represents a change in the market's framing — from "when will they cut?" to "do we need to consider a hike?" When that transition happens, the felt pressure on risk assets like Bitcoin escalates to an entirely different order of magnitude.

Not all forecasters agree. According to Reuters reporting, major brokerages still project two rate cuts within the year. But the same reporting noted that the Fed's own latest dot plot implies only a single 25bp cut. The divergence between broker forecasts and the Fed's own signaling creates an additional layer of uncertainty that the market must price.

One point that can be stated more clearly in text than was possible in the video: between rate cut expectations and actual cuts, there is a lag — and that lag is filled by macro data. Right now, the direction of that data is not friendly to cuts. If oil stays above $100, energy-driven inflation typically takes one to two months to show up in CPI. This means the April CPI (released in May) and May CPI (released in June) could both see energy components spike upward. The Fed has no reason to rush a cut in that environment.

What is pressuring Bitcoin is not an internal Bitcoin problem. It is the macro environment itself — one in which the Fed cannot comfortably ease. Oil rises, so inflation worries return. Inflation worries return, so the Fed stays put. The Fed stays put, so Bitcoin gets squeezed. Understanding this chain explains why even positive headlines fail to lift Bitcoin's price in the current regime.

3. The Anatomy of Selling Pressure: Whale Capitulation Meets Demand Absence

The video introduced Glassnode's whale selling data and CryptoQuant's demand contraction data separately. This post analyzes the structural outcome when the two operate simultaneously.

According to Glassnode's analysis, whale addresses holding between 100 and 10,000 BTC have been realizing large-scale losses during the recent price decline. On the Net Realized Profit & Loss 7-day EMA basis, daily losses exceeded $200 million — a pattern characteristic of capitulation selling. With Bitcoin already down over 52% from its peak, the emergence of whale position unwinding adds meaningful weight to the sell side.

CryptoQuant data cited by Bloomberg confirms that the demand side is failing to absorb this selling pressure. As of late March, Bitcoin's apparent demand — the amount of real buying in excess of new supply — was approximately negative 63,000 BTC. More Bitcoin is leaving or failing to be absorbed than is entering the market.

What the video did not have time to explore is the structural implication of these two data points working in tandem.

On the sell side, whales are accepting losses to exit positions. This is not routine profit-taking. It signals that at the large-holder level, the judgment "I'd rather take the loss now than risk further decline" has started to prevail. On the demand side, while ETFs and Michael Saylor's Strategy continue buying, their absorption capacity falls short of offsetting the total selling pressure in the market.

Breaking down the ETF data on a weekly basis makes this clearer. BeInCrypto's analysis shows that March ETF net inflows totaled $1.13 billion, ending a four-month outflow streak. The monthly figure looks positive. But week by week, March's third week saw only $95 million in inflows, and the final week flipped to negative $296 million. The headline monthly number was built on early-month inflows; the actual trend by month-end had already reversed.

The conclusion is the same one the video compressed into a single sentence: this market is not one where "institutions are buying, so it's fine." It is one where "institutions are buying, but they still can't overpower total selling pressure." Ignoring this structure and expecting a rebound based on sentiment alone will produce a persistent gap between expectation and reality.

One additional point that can be elaborated here: saying ETF inflows "returned" is very different from saying they are "sufficient." In the current market structure, stable weekly net inflows of at least $300–500 million would be needed to offset whale selling and demand contraction. The fact that the final week of March already flipped to outflows means ETF capital is also reacting sensitively to macro conditions. ETFs are a long-term ally for Bitcoin, but they should not be treated as a permanent short-term shock absorber.

4. Rebound Conditions: Not "What Gets Better" but "What Gets Less Bad"

The video presented CryptoQuant's scenario ($71,500–$81,200 potential rebound) and outlined three prerequisite conditions: Hormuz de-escalation, oil stabilization, and rate expectations holding. This post provides a more granular analysis of that rebound's character and limitations.

The CryptoQuant scenario published via The Block carries two essential points. First, Bitcoin demand remains in deep contraction. Second, despite that contraction, a de-escalation between the U.S. and Iran could trigger a short-term bounce to the $71,500–$81,200 range. Connecting these two statements makes it clear that the driving force behind any near-term rebound would be risk premium contraction, not demand recovery.

That distinction matters a great deal. A demand-driven rebound has durability. Trading activity picks up, fresh capital enters, on-chain metrics improve, and the price grinds higher over time. A risk-premium-contraction rebound, by contrast, is closer to a technical reflex — "conditions were terrible, now they're slightly less terrible." Such rebounds can arrive quickly, but without a change in the underlying demand structure, they tend to lack staying power.

BeInCrypto's April analysis identifies $67,000 as Bitcoin's most critical technical level. Throughout 2026, this level has functioned as a key support, with every dip below it being quickly reclaimed. However, with ETF and whale data weakening, a clean breakdown below $67,000 opens the path to $61,500 (the 0.382 Fibonacci level), followed by $60,000 as a psychological and technical floor.

Expanding on the three rebound conditions from the video:

Condition 1: Hormuz de-escalation. This does not require a full lifting of the blockade. A credible signal toward normalization — Iran expressing willingness to negotiate, U.S. Navy escort resumption, or major producers securing alternative shipping routes — could be sufficient. Since Trump's speech, the market has been waiting for such a signal, but none has materialized.

Condition 2: Oil stabilization. Brent settling below $100 would be ideal, but even a cessation of further upside within the $100–$110 range would begin to calm inflation fears. According to Bitcoin News analysis, Brent and WTI have been trading in a $99–$115 range, and narrowing of that range would constitute the first stabilization signal.

Condition 3: Rate expectations holding. "Holding" here means not slipping further. The market has already pushed the expected first cut to September. Any additional delay — or further growth in the probability of a hike — would compound the pressure on Bitcoin. Conversely, an April CPI print below expectations or dovish signaling from Fed officials could revive cut expectations and catalyze a short-term bounce.

The probability of all three conditions aligning simultaneously is not high at present. But even two of three would likely be enough to trigger a technical rebound. The risk lies in mistaking that rebound for a resumption of the structural bull trend. A bounce occurring while demand remains structurally weak can be reversed the moment conditions deteriorate again.

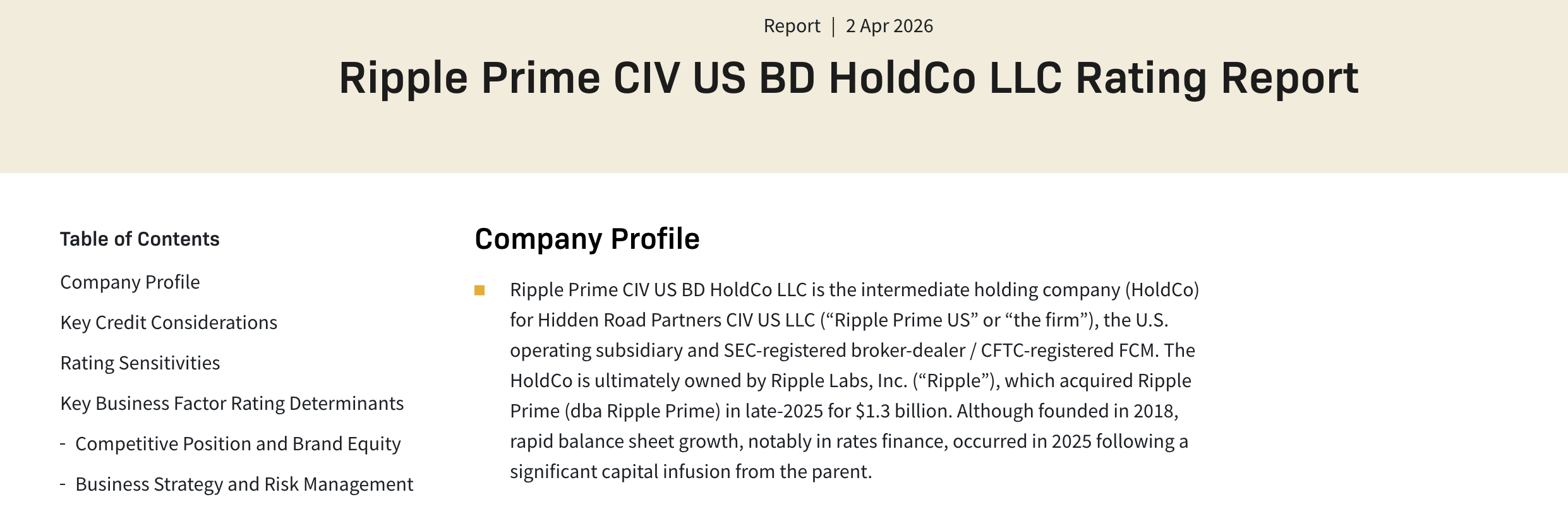

5. Ripple Prime BBB: The Structural Significance the Video Couldn't Fully Unpack

Time constraints in the video limited the Ripple Prime discussion to "a crypto company is starting to enter institutional financial language." This post covers the practical meaning of BBB, comparisons within the industry, the risks KBRA flagged, and the implications for XRP investors in considerably more detail.

5-1. What Is Ripple Prime?

Ripple acquired Hidden Road for $1.25 billion in 2025 and rebranded it as Ripple Prime. Hidden Road provided clearing, intermediation, and financing services across FX, digital assets, derivatives, swaps, and fixed income markets, clearing over $3 trillion annually and serving more than 300 institutional clients. Reuters reported that the deal made Ripple the only crypto company to own and operate a global multi-asset prime brokerage.

5-2. What a BBB Rating Actually Changes

KBRA assigned a BBB rating to Ripple Prime CIV US BD HoldCo and its primary operating subsidiary on April 2. BBB sits at the bottom of investment grade, but the gap between crossing that threshold and failing to is operationally significant. According to FinTech Weekly's analysis, pension funds, insurance companies, and banks select counterparties based on internal credit frameworks. Without an investment-grade rating, engaging with a counterparty requires a separate exception approval process. With one, the transaction falls within standard procedures. For Ripple Prime, BBB functions as a credential that opens the door to institutional clients.

The regulatory registrations and memberships of Ripple Prime US further define its character: SEC-registered broker-dealer, CFTC-registered FCM (futures commission merchant), FINRA and SIPC member, CME Group clearing member, and FICC Government Securities Division member. This list alone positions the news not as a crypto company's PR announcement but as something to be read within the language of institutional finance.

5-3. Rating Basis and Expansion Plans

KBRA noted that while Ripple Prime US is still in an expansion phase, it evaluated positively the exchange-traded derivatives (ETD) platform launched in 2024 and the fixed income repo business that reached meaningful scale in 2025, focused on short-duration U.S. Treasuries and agency securities. Backed by approximately $500 million in capital from Ripple Labs, the balance sheet grew significantly over the past 12 months and achieved profitability in 2025. An additional ~$500 million capital injection is expected in 2026.

The KBRA report also outlined expansion plans: Delta1 products — total return swaps and synthetic equity financing for leveraged ETF providers — as well as equity prime brokerage. KBRA viewed these as revenue diversification moves. This signals Ripple's intent not to remain a crypto broker but to ascend to a multi-asset prime brokerage spanning traditional finance.

5-4. Industry Comparison

Understanding how rare BBB is in crypto requires context. According to CryptoTimes reporting, Ledn, a Bitcoin lending platform, received a BBB- rating from S&P in early 2026. However, that rating applied to a specific structured product, not to Ledn as a corporate entity. Ripple Prime's BBB is an issuer-level rating — a fundamentally different category. Coinbase's corporate rating is also analyzed as sitting below Ripple Prime's. Direct comparisons have limitations, but a crypto-owned broker-dealer receiving an investment-grade issuer rating from an NRSRO (Nationally Recognized Statistical Rating Organization) is virtually unprecedented in the industry.

5-5. The Risks KBRA Flagged

This was mentioned in the video but deserves more explicit treatment in text. KBRA stated that Ripple's parent-level revenue is heavily driven by digital asset activity including XRP sales, making earnings vulnerable during a prolonged crypto downturn. This is a warning placed in an official credit rating document. The operating subsidiary itself runs a matched-book structure with no directional crypto exposure, but if the parent weakens, its capacity to provide capital support diminishes. Reading only the positive side of the BBB rating while omitting this warning produces a biased interpretation.

To elaborate further: Ripple Labs' primary revenue sources are XRP sales and digital asset-related services. A prolonged crypto bear market would erode XRP sale revenue, which in turn could affect the parent's ability to inject capital into Ripple Prime. KBRA's assessment that "parental support is expected to remain highly likely" reflects the current financial position, not a guarantee under all market conditions.

5-6. Implications for XRP Investors

Ripple Prime's BBB rating will not immediately lift the XRP price. Drawing a simple, direct line between the two makes the analysis shallow rather than deep. But viewed structurally, Ripple is no longer just a payments company. It is building an institutional financial stack that includes stablecoins (RLUSD), custody, prime brokerage, repo, and clearing. At the time of the Hidden Road acquisition announcement, Ripple also outlined plans to use RLUSD as collateral for prime brokerage products and to move portions of post-trade activity onto the XRPL for cost efficiency.

According to Cryptopolitan reporting, XRP is trading near $1.31, with limited recovery elasticity amid broad market weakness. The price is weak, but the structure is improving. That divergence is the core of the Ripple story right now. Price and structure do not always move in tandem. Markets often respond to structural change with a delay. But a situation where structure improves while price is suppressed can be more meaningful over the long run than a price rally unsupported by structural progress.

"BBB means XRP is going up" overstates the case. "It's just a company headline with no relevance to price" understates it. The balanced reading: Ripple is seriously expanding its institutional infrastructure business, and a credit rating agency has begun formally acknowledging that. At the same time, KBRA itself flagged parent-level XRP revenue concentration as a risk, and market prices remain under macro pressure — meaning this structural shift may not translate to short-term price action.

Conclusion: The Structure of Decline, the Structure of Recovery, and the Checkpoints

Bitcoin's fall below 67K was not random. Trump's speech failed to reassure the market. The Hormuz Strait risk pushed oil higher. As a result, rate cut expectations were pushed back — with the possibility of a hike entering the conversation. And Bitcoin's internal demand remained too weak to absorb the macro shock.

The structure of recovery is also identifiable. If Hormuz tensions ease, oil stabilizes, and rate cut expectations stop deteriorating, Bitcoin can attempt a technical rebound toward the $71,500–$81,200 range. But that rebound is conditional. In a market where demand is structurally weak, a single positive headline is unlikely to reverse the overall mood.

Ripple deserves separate attention. Even as the broader market gets compressed, the company is making meaningful progress in institutional financial infrastructure. Ripple Prime's BBB rating should be read as something far weightier than a headline-friendly catalyst. It is a signal of what kind of financial player Ripple is trying to become.

Four checkpoints to keep watching: First, where oil tops out. Second, how far rate expectations slide. Third, whether Bitcoin spot demand actually recovers. Fourth, whether institutional infrastructure news like Ripple Prime turns into follow-through numbers rather than one-time headlines. In turbulent markets, what lasts is never the most provocative sentence — it is these checkpoints.

FAQ

Q1. If Trump declares a ceasefire, will Bitcoin rebound immediately?

Not necessarily. Even if a ceasefire is announced, the practical normalization of Hormuz shipping, oil price stabilization, and rate expectation recovery each involve time lags. The market is more likely to respond to actual supply-chain normalization data than to a declaration alone. A ceasefire could trigger risk premium contraction, but it does not by itself change the demand structure.

Q2. If ETF inflows resume, will the decline stop?

The presence of ETF inflows matters less than their size and consistency. Under the current market structure, offsetting whale selling and demand absence would require stable weekly net inflows of at least $300–500 million. Given that March's final week already flipped to outflows, ETFs are a long-term positive but cannot be relied upon as a short-term stabilizer.

Q3. What impact does Ripple Prime's BBB rating have on the XRP price?

In the short term, the impact is limited. The BBB rating applies to the Ripple Prime broker-dealer subsidiary, not to the XRP token. Structurally, however, it signals that Ripple is upgrading its institutional financial infrastructure — and plans like RLUSD collateral usage and XRPL post-trade migration could create long-term positive effects on the XRP ecosystem if realized. The key variables are time and data.

Q4. Could a rate hike actually happen?

It is not the base case at present. Major brokerages still project rate cuts within the year. However, the fact that December hike probability has climbed to 25% signals that the market is taking oil-driven inflation re-acceleration seriously. For a hike to materialize, CPI would need to significantly exceed expectations for several consecutive months — and that probability depends heavily on the Hormuz situation.

Source Table

| Tier | Source | Type |

|---|---|---|

| Primary | KBRA — Ripple Prime Rating Report (Apr 2, 2026) | Credit Rating Report |

| Primary | BeInCrypto — Bitcoin Price Prediction April 2026 | Market Analysis (ETF/On-chain) |

| Primary | Yahoo Finance — Bitcoin Price Data | Price Data |

| Secondary | CryptoTimes — Ripple Prime BBB Rating Analysis | Rating Commentary |

| Secondary | FinTech Weekly — Ripple Prime Institutional Impact | Institutional Analysis |

| Secondary | Cryptopolitan — KBRA Assigns BBB to Ripple Prime | Rating Coverage |

| Secondary | Bitcoin News — Hormuz Supply Disruption and VIX | Macro Analysis |

| Secondary | CoinCu — Kroll Rates Ripple Prime BBB | Rating Commentary |

| Contextual | CryptoSlate — Bitcoin April 2026 Performance | BTC Dominance/Outlook |

| Contextual | Fortune — Bitcoin Price April 2026 | Price Coverage |

Investment Disclaimer

This post does not constitute a recommendation to buy or sell any asset. All forecasts, analyses, and data are provided for informational purposes only and should not be used as the sole basis for any investment decision. Cryptocurrency investment involves significant risk, including possible loss of principal. Please consult an independent financial advisor before making any investment decisions.

![[마켓 분석] 비트코인 8만 달러 앞에서 멈춘 시장](https://storage.ghost.io/c/8c/af/8caf2296-06bf-4501-ae99-5e72cb676b76/content/images/size/w600/2026/04/63d9df35-5d28-48fe-9a7a-3f651c82aafe.png)