Same Market, Different Price Engines

BTC runs on ETFs and macro. ETH runs on on-chain infrastructure. XRP faces a gap between Ripple's expansion and token demand. With Standard Chartered's $500K/$40K forecasts and Ripple entering the $13T treasury market, we analyze why three assets

What You See When You Put Bitcoin, Ethereum, and XRP in One Frame

DATA BOX

BTC Standard Chartered 2030 target: $500,000 | Current price: ~$66,000 | BTC dominance: 58.16% | Late March–early April ETF daily flows swinging between -$226M and +$117M

ETH Standard Chartered 2030 target: $40,000 | Current price: low $2,000s | Ethereum RWA distributed asset value: $15.54B | Stablecoin market cap: $168.27B | ETH/BTC ratio: ~0.03

XRP Current price: $1.33 | 6 consecutive months of decline (since Oct 2025), cumulative -55% | Ripple Treasury 2025 client payment volume: $13T | Hidden Road annual clearing: $3T+ | KBRA BBB rating assigned (Apr 2, 2026)

Bitcoin remains the benchmark of the crypto market, but its price engine is now far more tethered to ETFs and macro variables than it used to be. Standard Chartered's Geoff Kendrick maintained his $500,000 Bitcoin target but pushed the timeline to 2030, citing a shift in future demand from corporate balance sheets to ETF-driven institutional flows. Meanwhile, daily flows into U.S. spot Bitcoin ETFs have been swinging sharply between large inflows and outflows in late March and early April.

Ethereum's price action looks frustrating, but its centrality as on-chain financial infrastructure remains overwhelming. As of early April, the Ethereum network's RWA-related distributed asset value stands at roughly $15.5 billion, with a stablecoin market cap of approximately $168.3 billion. Yet ETH/BTC sits around 0.03, and mainnet fee revenue is being eroded by competing networks and L2 growth. The infrastructure is strong, but the price premium has not been fully restored.

Ripple is expanding aggressively into corporate treasury and prime brokerage. Ripple Treasury processed $13 trillion in client payment volume in 2025, and Hidden Road clears over $3 trillion annually with more than 300 institutional clients. KBRA assigned Ripple Prime a BBB rating. And yet XRP has fallen for six consecutive months since October 2025, losing over 55% of its value. That disconnect is the key to understanding XRP right now.

In the video, the constraint was time — getting across the big picture that "these three assets work differently" as quickly as possible. In this blog post, there is room to unpack that sentence more carefully. The most interesting part of today's market is not the gap between bullish long-term forecasts and bearish current prices. What matters more is why that gap exists. Bitcoin has become the entry gate for institutional capital. Ethereum has become the rail on which actual financial services operate. And XRP is caught in a situation where the company's expansion and the token's value capture are moving at different speeds. They sit in the same market, but they cannot be evaluated the same way.

To understand this, one thing has to be acknowledged first. The crypto market no longer operates on a "good news lifts all boats" model. Bitcoin must be read through the lens of ETFs and interest rate expectations. Ethereum through stablecoin and tokenization infrastructure and its value accrual logic. XRP through whether Ripple's business expansion actually translates into token demand. My read is that the market is now assigning fundamentally different multiples to these three assets. Rather than three members of the same sector, they are closer to three distinct narratives, each carrying different cash flow expectations and risk premiums.

1. Bitcoin: Not "the Strongest Coin" but "the Most Institutionalized Coin"

The best starting point for understanding Bitcoin today is the fact that it now behaves far more like a macro asset than it used to. In Standard Chartered's updated outlook, Kendrick kept the $500,000 target but moved the timeline to 2030, reasoning that future buying would be driven more by ETFs than by corporate treasuries. That sentence matters more than the price target itself. It signals that Bitcoin's long-term narrative has shifted from the abstract metaphor of "digital gold" to the more concrete thesis of "the gathering point for institutional capital flowing in through ETFs."

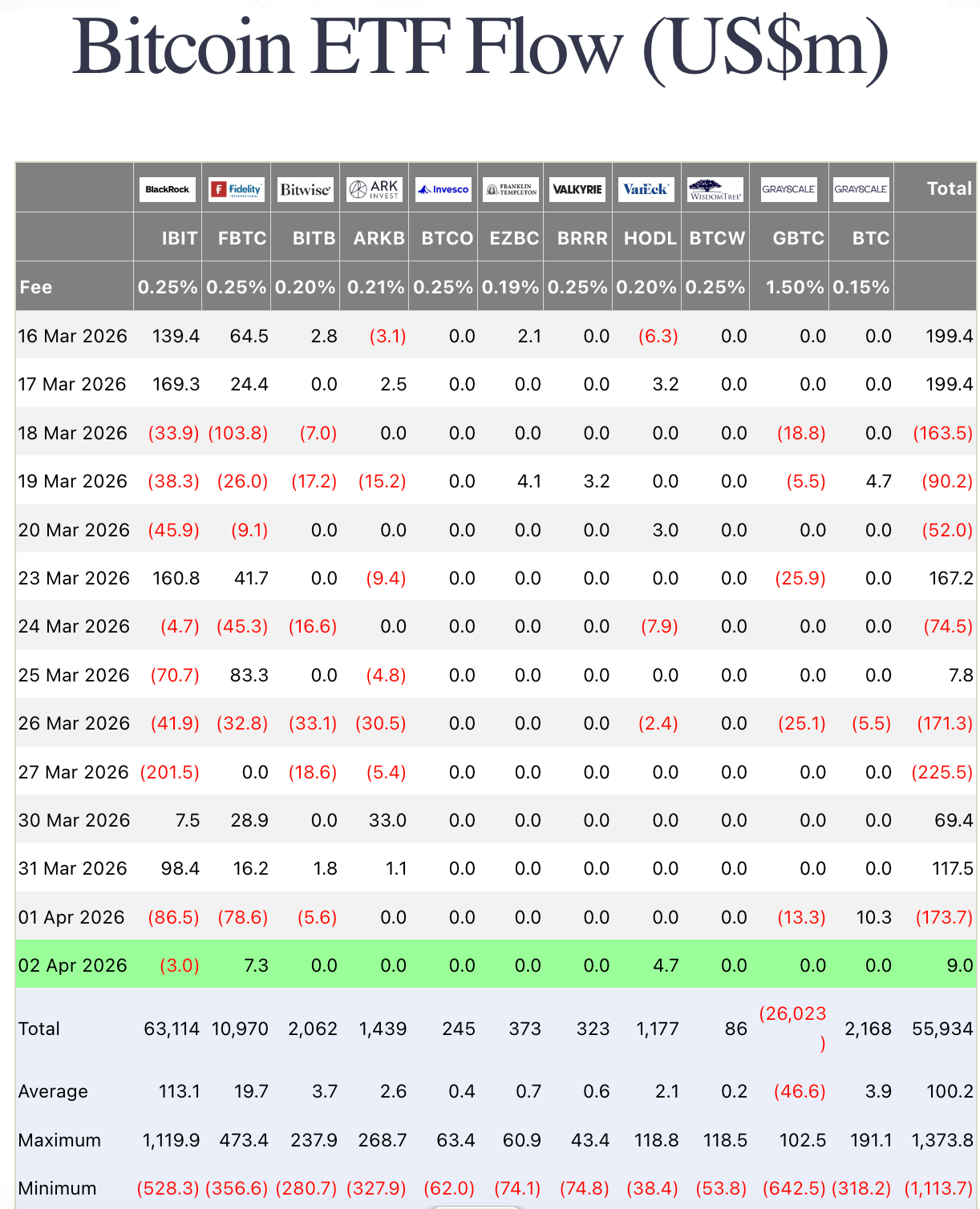

Actual fund flows support this interpretation. According to Farside Investors (an ETF flow tracking platform), U.S. spot Bitcoin ETFs recorded a $225.5 million net outflow on March 27, then bounced back with $69.4 million in net inflows on March 30 and $117.5 million on March 31. But on April 1, they swung back to a $173.7 million net outflow. This shows that ETFs are no longer a one-directional bullish story. Institutional money flows into Bitcoin when markets calm down, but exits just as quickly when anxiety returns. ETFs are a long-term ally for Bitcoin, but they should not be mistaken for a permanent shock absorber for short-term prices.

Bitcoin dominance holding at elevated levels tells the same story. As of early April, Bitcoin dominance stood at 58.16%. This figure does not reflect a bullish market aggressively buying altcoins. It more likely reflects capital within crypto gravitating toward the least risky option when uncertainty rises. In other words, current Bitcoin strength carries a meaningful "risk-averse preference" component rather than pure market-wide optimism. Missing this distinction leads to the mistake of equating Bitcoin's resilience with overall market health.

The key takeaway here is this: Bitcoin no longer moves on pure crypto narratives alone. Variables like the dollar, oil prices, rate expectations, and ETF flows now feed directly into its price. That means reading Bitcoin requires looking at macro conditions and capital allocation structures before looking at project-level news. This is what it means for Bitcoin to have matured — and also what it means for it to no longer be a comfortable asset. The most institutionalized coin is the first to absorb institutional shocks. That paradox defines Bitcoin today.

2. Ethereum: The Network Is Strong — So Why Is the Price So Sluggish?

Ethereum is best understood from the opposite direction. If Bitcoin is "the gate where money enters," Ethereum is "the rail where money actually moves." Standard Chartered's forecast placed Ethereum at $40,000 by 2030, noting that tokenization, stablecoins, and institutional blockchain deployment would initially settle on Ethereum more than on other chains. The key question is not short-term price but which base infrastructure traditional finance chooses first when moving on-chain. So far, the answer still leans toward Ethereum.

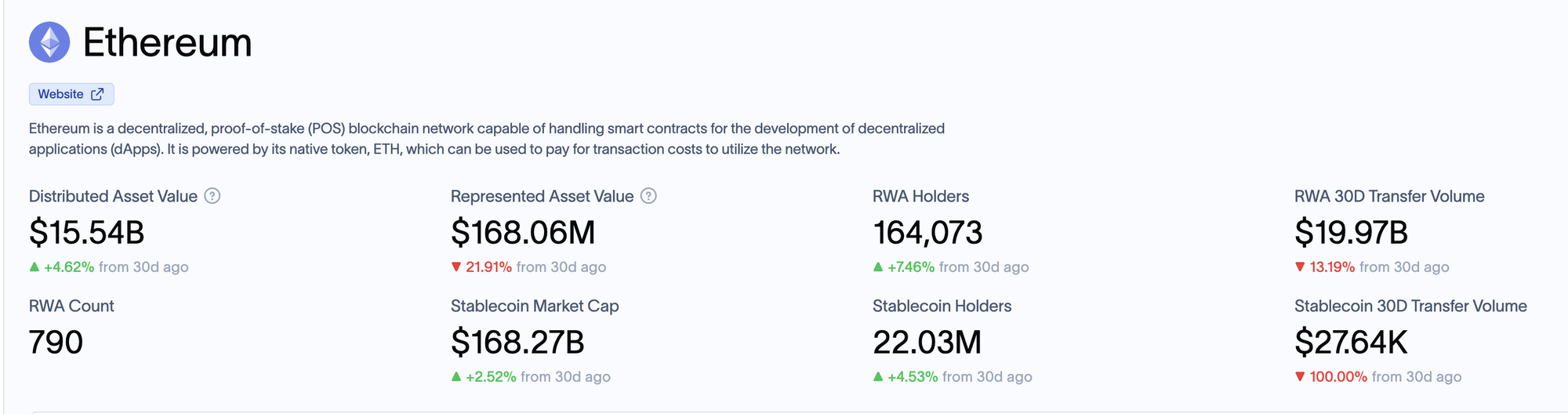

The data backs this up fairly clearly. As of early April, RWA.xyz shows the Ethereum network's distributed asset value at approximately $15.54 billion, stablecoin market cap at roughly $168.27 billion, and stablecoin holders at about 22.03 million. This is not simply a story about Ethereum being large. These numbers reveal where tokenized real-world assets and dollar-based digital liquidity are most deeply concentrated. A network is not just a technology platform — it is a place where capital actually settles. On that measure, Ethereum still holds the lead.

The problem is how effectively that infrastructure strength converts into ETH price. This is exactly where the Ethereum narrative stalls. CoinDesk recently reported that while Ethereum hosts more than half of global stablecoin supply, its base layer's fee and revenue share is being eroded by competing networks and L2 growth. In other words, a lot is happening on Ethereum, but the economic fruit of that activity is not fully accruing to ETH itself. A structure is forming in which technology usage and token price do not move in lockstep.

The ETH/BTC ratio captures this tension well. CoinDesk reported a figure of 0.02923 in February, and Standard Chartered's recent ETH bull case also starts from the premise that the current ratio sits around 0.03 — a low base. The market acknowledges Ethereum's infrastructure value but is not yet willing to translate that value into a premium on par with Bitcoin. The issue is not that "the infrastructure is weak." It is that the explanation for how that infrastructure strength maps to ETH value has not yet fully convinced the market.

So when looking at Ethereum, two questions need to be tracked simultaneously. First, are stablecoins and tokenized assets continuing to accumulate on Ethereum? Second, is that accumulation actually translating into ETH value capture through mechanisms like mainnet fees, burn rates, and security premiums? The answer to the first question remains fairly positive. The answer to the second is where the market remains reserved. That gap between the two is what explains the current ETH price. It is why the infrastructure looks strong but the price looks stuck.

3. XRP: The Company Is Growing — So Why Is the Token Getting a Cold Reception?

This is the most important section of this post. In the video, time constraints limited the XRP discussion to "you need to separate the company from the token." In text, there is space to lay out that structure more explicitly. Ripple is currently executing a very aggressive business expansion. Ripple Treasury's April 1 announcement introduced Digital Asset Accounts and Unified Treasury — features that allow corporate treasury teams to view and manage fiat and digital assets in real time within a single system. Ripple described this as "the first time native digital asset capabilities have been embedded in an enterprise TMS."

The weight of this announcement lies in its context, not just its features. After acquiring GTreasury, Ripple layered digital asset functionality onto 40-plus years of enterprise treasury management infrastructure. The company stated that Ripple Treasury processed $13 trillion in client payment volume in 2025, spanning SMEs to Fortune 500 firms. It also cited its own 2026 survey of more than 1,000 global treasury leaders, in which 72% said digital asset solutions were necessary to remain competitive. This positions Ripple not as "a token company for investors" but as "an enterprise treasury infrastructure provider" — a deliberate redefinition.

The Hidden Road acquisition takes that picture a step further. According to Reuters and Hidden Road's official announcement, Ripple agreed to acquire Hidden Road for $1.25 billion in 2025. Hidden Road was clearing $3 trillion annually and serving over 300 institutional clients. Reuters noted that the deal made Ripple the only crypto company to own and operate a global multi-asset prime brokerage. The use of RLUSD as collateral for prime brokerage products was also highlighted. This signals Ripple's intent to unify payments, stablecoins, prime brokerage, and clearing into a single institutional financial stack.

KBRA's assignment of a BBB rating shows that this expansion is entering market-friendly institutional language. On April 2, KBRA assigned BBB to both Ripple Prime and its primary operating subsidiary, noting that the entity is an SEC-registered broker-dealer, CFTC-registered FCM, FINRA and SIPC member, and CME Group clearing member. According to related reporting, Ripple held approximately $5 billion in cash as of Q3 2025 and more than 40 billion XRP. This is far heavier than a typical press release. A credit rating agency is translating "corporate fitness" into institutional language.

Here is where it gets complicated. If the company is growing like this, why is the token not following? CryptoSlate reported on April 2 that XRP had fallen for six consecutive months since October 2025, with a cumulative decline exceeding 55% and a price of $1.33 at the time of writing. It also noted that Binance's 30-day liquidity index for XRP had dropped to approximately 0.062, with 30-day turnover at roughly $4.46 billion. The market is aware of Ripple's enterprise expansion but has not yet translated that awareness into spot XRP buying demand or liquidity recovery.

The most important interpretation here is captured in a single line from CryptoSlate: infrastructure usage and token buying are not the same thing. Even if corporations use Ripple Treasury, institutions use Hidden Road, and RLUSD serves as collateral, none of that automatically generates spot XRP purchases. In the video, this point was covered briefly. In text, it can be stated more directly. XRP's current problem is not that the company lacks execution. It is that the market has not yet been persuaded how that execution accrues to token value.

The Crypto Basic's discussion of whether global banks would realistically adopt XRP at scale given Ripple's large token holdings is an expression of exactly that skepticism. The article leans more toward community debate than rigorous research, but the question itself is hard to dismiss. Large financial institutions do not evaluate technology alone. They weigh token distribution, volatility, liquidity, governance, and regulatory risk together. And the counterargument that stablecoins like RLUSD may be more practical as payment instruments — given their lower price volatility — is entirely legitimate. So the future of XRP is less about "Ripple succeeds, therefore XRP rises" and more about at what point Ripple's infrastructure expansion creates genuine demand that requires XRP specifically.

The debate around XRP is better understood not as a fight between bulls and bears, but as market reserve toward a value capture mechanism that has not yet been sufficiently validated. The company is growing, but the token is not being credited proportionally. This state of affairs could persist indefinitely, or it could resolve quickly once specific real-usage data materializes. What matters is not sentiment but data. Until enterprise treasury adoption, prime brokerage growth, and RLUSD collateral usage demonstrably create XRP liquidity demand in some measurable form, the market's discount is likely to continue.

4. What Changes When You Look at All Three Together

The reason for covering these three assets in one post is not simple comparison. It is that within the same market, the way money enters, the way money stays, and the way value accrues are all different. Bitcoin is a function of ETFs and macro. Ethereum is a function of network centrality and value capture. XRP is a function of corporate expansion and token accrual mechanics. Applying the same yardstick to all three consistently produces the wrong answer.

The checkpoints must therefore be different. For Bitcoin, watch ETF net flows, the dollar, and rate expectations. For Ethereum, watch whether RWA and stablecoin balances continue to grow on-chain — and whether that growth converts into ETH value capture. For XRP, watch whether Ripple's enterprise and institutional infrastructure expansion creates a structure that generates actual XRP demand. That distinction alone provides far better explanatory power for why three assets in the same market react differently to the same news on the same day.

Ultimately, the core task right now is not choosing between optimism and pessimism. It is distinguishing the conditions under which each asset can be re-rated. Bitcoin needs macro easing and ETF stabilization. Ethereum needs a catalyst that translates its strong infrastructure into price premium. XRP needs empirical proof that Ripple's business expansion converts to token demand. The fact that the questions are this different within the same crypto market is, paradoxically, the most accurate description of where the market stands today.

FAQ

Q1. If the long-term outlook for Bitcoin is intact, can short-term corrections just be ignored?

Not quite. Long-term forecasts describe the directional pull of demand structures, but short-term prices are heavily influenced by ETF flows and macro conditions. The fact that ETF capital swung between large inflows and outflows within days in late March and early April shows that Bitcoin remains an extremely sensitive asset in the short term, regardless of its long-term trajectory.

Q2. Ethereum has strong infrastructure — so why is the price always so frustrating?

Because network activity and token value capture are not the same thing. Ethereum is the center of stablecoins and tokenized assets, but the base layer's fee and revenue share is being eroded by competing networks and L2 expansion, leaving the ETH price premium insufficiently restored. The infrastructure strength is clear, but the pathway from that strength to ETH price recovery is still being debated.

Q3. What is the key risk for XRP?

Not the institutional expansion itself, but the fact that the expansion does not automatically connect to XRP token value. Ripple is aggressively building out corporate treasury and prime brokerage infrastructure, but the market does not yet see that as directly translating to increased spot XRP demand. The critical variable for XRP is not just whether Ripple's business succeeds, but how that success gets translated into token demand and liquidity.

Q4. Which of the three should investors focus on first?

The point is not that one asset deserves priority over the others. It is that each requires a different set of variables to watch. For Bitcoin: ETF flows, dollar strength, and rate expectations. For Ethereum: stablecoin and RWA balance growth plus mainnet value capture. For XRP: whether Ripple's infrastructure expansion actually generates token demand. The reason these three assets react differently to the same market conditions on the same day traces directly back to these divergent checkpoints.

Source Table

| Tier | Source | Type |

|---|---|---|

| Primary | KBRA — Ripple Prime Rating Report (Apr 2, 2026) | Credit Rating Report |

| Primary | Ripple — Digital Assets in Every CFO's Toolkit (Apr 1, 2026) | Official Corporate Release |

| Primary | RWA.xyz — Ethereum Network Dashboard (as of Apr 2, 2026) | On-chain Data |

| Secondary | The Crypto Basic — Standard Chartered $500K BTC / $40K ETH (Apr 2, 2026) | Forecast Coverage |

| Secondary | CryptoSlate — XRP Six-Month Decline Analysis (Apr 2, 2026) | Market Analysis |

| Secondary | Farside Investors — US BTC ETF Flow Data | ETF Flow Tracking |

| Secondary | CoinDesk — Ethereum Fee and Value Capture Analysis | Research Coverage |

| Secondary | FinTech Weekly — Ripple Prime Institutional Impact | Institutional Analysis |

| Contextual | The Crypto Basic — Why Would Banks Use XRP (Apr 2, 2026) | Community Debate |

| Contextual | CryptoTimes — Ripple Prime BBB Analysis | Rating Commentary |

Investment Disclaimer

This post does not constitute a recommendation to buy or sell any asset. All forecasts, analyses, and data are provided for informational purposes only and should not be used as the sole basis for any investment decision. Cryptocurrency investment involves significant risk, including possible loss of principal. Please consult an independent financial advisor before making any investment decisions.

![[마켓 분석] 비트코인 8만 달러 앞에서 멈춘 시장](https://storage.ghost.io/c/8c/af/8caf2296-06bf-4501-ae99-5e72cb676b76/content/images/size/w600/2026/04/63d9df35-5d28-48fe-9a7a-3f651c82aafe.png)