Is XRP a Bank Coin or a Market Coin?

XRP's future cannot be explained by "banks adopt it, price goes up." The real question is whether institutional payment demand and XRPL's native DEX liquidity can connect.

The growing gap between Ripple's business narrative and XRPL's original vision

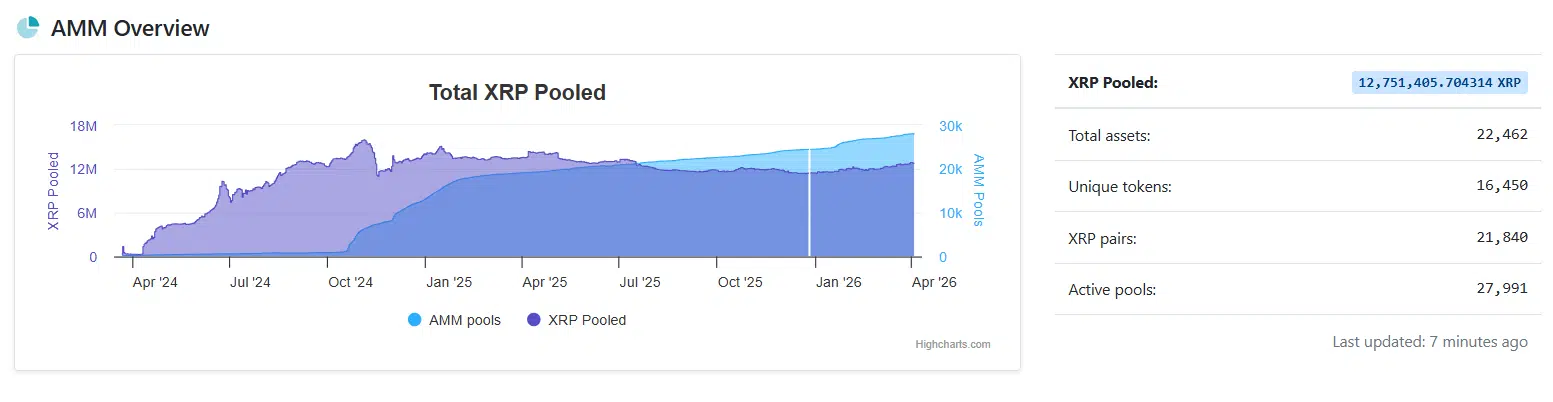

XRP's future cannot be explained with a single line like "it goes up when banks adopt it." The more precise question is this: when real institutional payment demand enters, does XRPL — as a public market infrastructure — possess deep enough liquidity to absorb that demand without destabilizing impact? Right now, roughly 28,000 active AMM pools operate on XRPL, with native DEX daily trading volumes ranging between $450 million and $600 million. Tokenized real-world assets (RWAs) on the network have reached $2 billion. Yet the most common sentence used to describe XRP remains: "the coin for bank remittances." That gap is where this analysis begins.

This piece does not treat four recent XRP-related developments as a simple collection of bullish headlines. Instead, it reframes them around a more fundamental question: XRP's identity is splitting again, and how we resolve that split determines how we should value the asset going forward. The starting points are four articles published by The Crypto Basic, but the structural backbone of this analysis leans on XRPL's official documentation, public announcements, and the verifiable intent behind original statements — because what matters now is not headline sensationalism, but the deeper question of what kind of asset XRP should be understood as.

DATA BOX — OVERVIEW

FACT XRPL's official documentation describes XRP as the native asset of the XRP Ledger, created in 2012 for payments. It simultaneously identifies XRPL as an open-source, permissionless, decentralized blockchain, and explicitly separates Ripple as a technology company independent from XRP. The XRPL DEX has been in continuous operation since the 2012 launch, and AMM functionality is already integrated into that DEX to provide liquidity. Meanwhile, The Crypto Basic reports that Pano Mekras argues XRP should be seen not as "a banking tool" but as "a decentralized commodity on a democratic network." SBI Ripple Asia and DSRV have begun joint research on XRPL-based remittance and payment use cases for the Japan–Korea corridor. And David Schwartz has clarified that his longstanding "XRP can't be dirt cheap" remark was a payment efficiency observation, not a price prediction.

INTERPRETATION Thread these pieces together and the conclusion is straightforward: XRP's future is not adequately explained by "bank adoption" alone. The more accurate question is whether institutional payment demand and XRPL's internal public liquidity market can connect. Ripple's business strategy has long been institution-centric — that is true. But that alone does not fully define what XRP is. XRPL itself has been an open network with embedded market structure since inception.

IMPLICATION Evaluating XRP therefore requires moving beyond the one-dimensional "banks use it, price goes up" thesis. If institutional payment narratives survive but the market remains shallow, shock absorption fails. If the DEX and AMM are active but no real payment demand connects, structural expansion stalls. The core variable is not price itself, but the liquidity and usage context that supports price.

PLAN A / PLAN B Plan A: XRP simultaneously connects institutional payments and XRPL's native liquidity market. In this scenario, real-world corridor research (Japan–Korea), XRPL Payments expansion, DEX/AMM liquidity deepening, and DeFi primitive additions like XLS-66D reinforce each other. Plan B: institutional narrative persists, but native market depth fails to develop sufficiently. In this case, XRP may remain "an asset with many good stories" without accumulating self-sustaining network value.

Bottom line XRP's real battleground is not bank adoption per se, but whether XRPL as a public market can absorb real payment demand with sufficient depth and stability.

1. Why is XRP's identity becoming a problem again?

The most interesting shift around XRP right now is not price action — it is an axis rotation in how the asset gets interpreted. For years, XRP has been publicly understood through a narrow set of images: "bank coin," "remittance coin," "bridge asset." The argument now resurfacing is whether this frame is too restrictive to capture everything XRP actually is. Pano Mekras has argued that XRP should not be confined to a bank-centric narrative and that its identity needs to be restored to that of a public network asset. This is not mere community sentiment — it is closer to a structural proposal: separate Ripple's business narrative from XRP's network identity, and evaluate them independently.

Why this matters is that it changes the question investors ask. Instead of only watching "which bank did Ripple sign," it forces a parallel question: "what kind of market structure is growing inside XRPL?" This is not a bullish-or-bearish question. It is an analytical framework upgrade. When markets interpret an asset narrowly, price gets pulled around by individual headlines. When markets begin evaluating an asset structurally, they start seeing mechanisms before they see price. XRP is standing at exactly that transition point.

2. Was XRP ever really a bank coin?

The official documentation answers this first. XRPL's introduction page describes XRP as the native digital asset of the XRP Ledger — an open-source, permissionless, decentralized blockchain. It states that XRP was created in 2012 for payments, can be sent directly without a central intermediary, and is designed for use cases including cross-border payments and micropayments. Read literally, XRP's origin point is clearly "payments." But that does not automatically mean "bank-exclusive." The official language actually leans the opposite direction: an asset that can be transmitted directly without intermediaries, operating on an open network.

Equally important is that XRPL explicitly separates itself from Ripple. The official page states that Ripple is a technology company, and XRP is an independent digital asset. XRPL itself is described as a "decentralized public blockchain built for business," with network operations open to anyone and consensus achieved through multiple validators. This distinction matters because it means that reducing XRP's entire identity to Ripple's business strategy is not structurally accurate. XRP serves as a Ripple business tool, but it exists first as the native asset of an open public network.

The honest answer to "what was XRP originally" is neither bank coin nor fully anti-institutional coin. The more precise statement is: XRP was originally a payment asset operating on an open network, and institutional payments were one of its use cases — not its defining boundary. Inverting that sequence narrows the identity.

3. Why did the market end up remembering XRP as a 'bank coin'?

Market memory is typically shaped more by business narratives than by technical documentation. Ripple spent years pushing a strong message centered on financial institutions, cross-border payments, and enterprise payment rails. It was natural for the market to internalize the idea that XRP derives value primarily from bank adoption. Mekras, through The Crypto Basic, criticized this exact dynamic — arguing that the bank-centric frame has obscured XRP's original vision. He frames the institutional push as an adoption strategy that can be acknowledged, but should not be mistaken for XRP's identity itself.

This distinction is worth pausing on. The "bank coin" frame is not entirely wrong. But it may have hardened to a degree that obscures XRPL's other structural dimension. Because XRPL is not only a payment network — it has featured a built-in DEX since inception. XRPL's official documentation states that the DEX has been in continuous operation since the 2012 launch, allowing users to trade XRP and other tokens with minimal network fees. Viewing XRP as nothing more than a "bank coin" means missing a market function that has existed from day one.

The most consequential side effect of the bank coin frame is that it reduced XRP's success criteria to a single variable. Many investors ended up watching only whether Ripple signed bank deals, while the broader value axes — XRPL's market structure, tokenization capabilities, on-chain liquidity, native exchange activity — received comparatively less attention. In retrospect, those overlooked structural elements may be what matters most in the long run.

4. What does the SBI Ripple Asia–DSRV research actually signal?

None of this means institutional payment narratives should be discarded. In fact, the SBI Ripple Asia–DSRV joint research says the opposite. According to The Crypto Basic, SBI Holdings CEO Yoshitaka Kitao personally confirmed that SBI Ripple Asia and South Korean blockchain infrastructure firm DSRV have begun joint research exploring XRPL's potential for remittance and payment use cases across the Japan–Korea corridor. The focus areas are regulatory alignment, operational design, integration with existing financial infrastructure, and XRPL's settlement capabilities. The article explicitly characterizes this as early-stage research — not a product launch or confirmed commercial deployment. But the signal is clear: institutional exploration of XRPL as payment infrastructure is ongoing, particularly in East Asian corridors.

This makes the XRP narrative more three-dimensional. Markets tend to force binary choices — "institutional or public network" — but reality suggests both axes can coexist. The same article notes that both Japan and South Korea are advancing regulatory frameworks around stablecoins and blockchain financial services. Regulatory design differences between the two countries present alignment challenges, but viewed from the opposite angle, the very fact that regulatory environments are taking shape is what makes such joint research possible. The study covers four key areas: identifying challenges arising from differences in each country's financial systems, mapping relationships with existing remittance infrastructure, evaluating technical and operational hurdles for blockchain adoption, and exploring long-term application opportunities.

To be blunt, this research represents a list of verification tasks more than a basis for enthusiasm. Regulation, operations, integration, stability — real-world implementation passes through layers far more complex than narrative. The appropriate reading is not "adoption confirmed" but rather "institutional payments remain a live area of realistic examination." And that alone is significant, because it shows that XRP's future may still be determined at the intersection of real payment demand and market liquidity.

5. What does David Schwartz's statement actually mean?

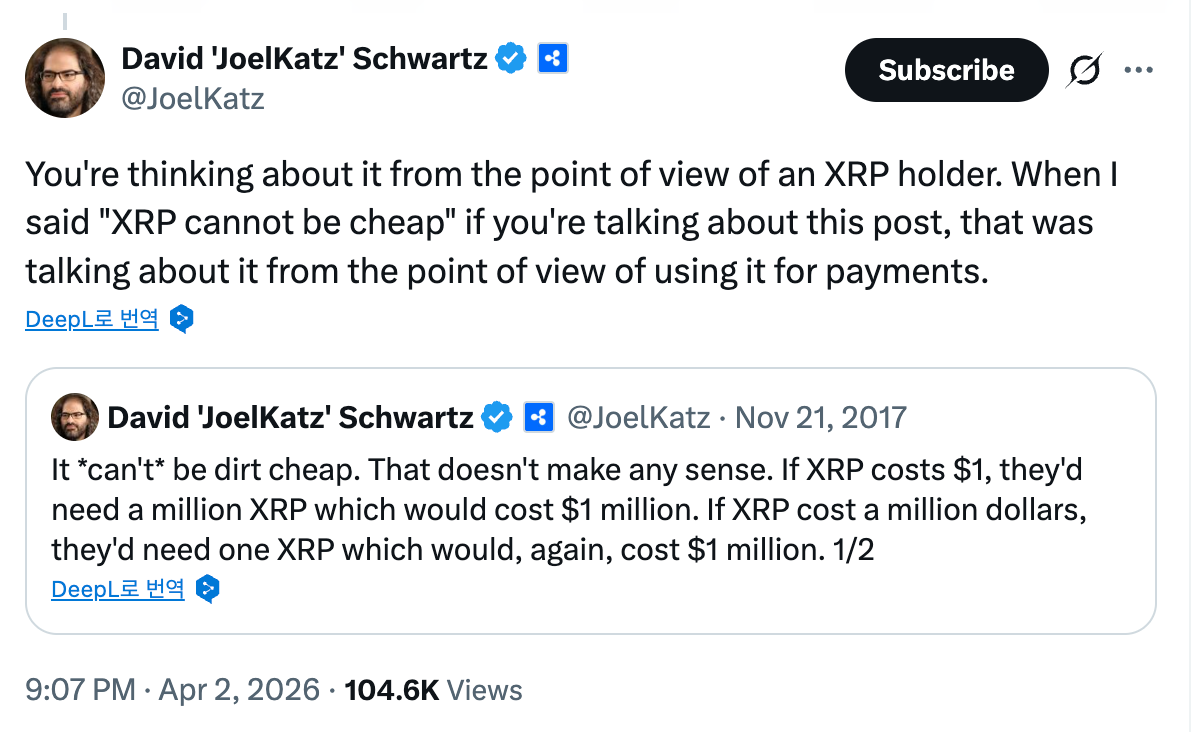

David Schwartz's remark that "XRP can't be dirt cheap" has been consumed by the community for years as a kind of price prophecy. But according to The Crypto Basic, Schwartz recently re-explained the statement, clarifying that the original intent was from a payment point of view. The comment was first made in November 2017, when XRP traded at $0.24.

The logic is straightforward. When institutions use XRP to move large sums, what matters is the total value being transferred, not the number of tokens involved. If $1 million needs to be sent, it requires 1 million XRP at $1 per token, or just 10,000 XRP at $100 per token. The total cost is identical. The difference lies in market impact — absorbing 1 million tokens at once exerts entirely different liquidity pressure than absorbing 10,000. In the same article, Schwartz used Bitcoin as an analogy: when BTC traded around $300, large transactions could significantly move the market price, but as its price rose, the market absorbed large trades far more smoothly. XRPL validator Vet also noted that people have been misinterpreting the remark as a price prediction, when it is fundamentally a structural explanation about payment utility.

The center of this logic is not investment return — it is payment efficiency and market impact minimization. Most people approach price with consumer-goods intuition: cheaper is better for use. But payment assets work differently. If the goal is large-scale value transfer, a unit price that is too low combined with a shallow market means more tokens are needed, amplifying market shock. Schwartz's argument is not "XRP must be expensive" but rather that for XRP to function as a payment asset, price and liquidity must be reinforced together. For reference, XRP has risen from $0.24 in 2017 to approximately $1.32 today — roughly a 450% increase. This level may be adequate for current payment volumes, but if transaction scale expands significantly, price would need to adjust accordingly.

This matters because it loops back to liquidity. High price with a shallow market is meaningless. Deep market with no demand is equally weak. Schwartz's statement, properly read, suggests not a moon price but a system where price, market depth, and payment efficiency are structurally interconnected.

DATA BOX — XRPL ON-CHAIN SNAPSHOT

Quantitative growth is confirmed. However, as the same reporting notes, many pools still lack sufficient capital depth to absorb large trades without significant slippage. Pool count stands at 28,000 — but individual pool capital depth remains a work in progress.

6. Why does XRPL native DEX liquidity matter so much?

The most hyperbolic expression in this cluster of developments is "game over." But the core argument behind the hyperbole is serious. The Crypto Basic quoted XRPL validator Vet as claiming that once the native DEX bootstraps deep liquidity with high-quality assets, the competitive picture changes fundamentally. That exact phrasing should not be taken at face value, but understanding why such a statement emerges is important. XRPL has had a built-in DEX since 2012, and AMM functionality has been activated as an integrated extension of that existing exchange.

XRPL's official documentation explains that AMMs provide liquidity to the DEX, and that individual trades can automatically use order books only, AMMs only, or a hybrid of both — selecting whichever route offers the better rate. The system is designed to optimize for the cheapest execution path. And fundamentally, AMMs reduce slippage as pool size grows. Deeper pools mean large trades cause less price disruption; shallow pools mean even small trades can move prices significantly. Whether for payments or trading, efficiency is ultimately determined by market depth.

The structural implication is substantial. XRPL's future depends not merely on "who uses XRP" but on how thick a market can be built inside XRPL itself. Even if institutional payment demand materializes, shallow markets reduce efficiency. Even if the public network is active, shallow liquidity pools limit utility. Payments and markets converge at liquidity. This is precisely where the institutional payment narrative and the public market narrative stop competing and start merging into a single structural question.

7. What does XLS-66D reveal about XRPL's expansion trajectory?

A proposal to deepen liquidity more organically is already on the table. According to the XRPL blog, the XLS-66D specification aims to introduce a native lending protocol to XRPL — an on-chain fixed-term loan structure targeting durations of approximately 30 to 180 days. It would operate through pooled assets in Single Asset Vaults built on XLS-65D. Per the same article, the proposal is currently before XRPL's 34 dUNL validators for voting, but support remains low as validators exercise caution over security. Vet has advised the community to review the proposal thoroughly before approval.

The significance of this protocol lies less in whether it passes and more in the direction it represents. XRPL's ecosystem is moving beyond payments and simple exchange toward broader DeFi primitives: lending, vaults, capital efficiency tools. This kind of expansion, if successful, is what allows DEX liquidity to deepen organically rather than depending solely on external capital inflow. The same article notes that firms like Evernorth are already preparing for the protocol's activation.

In the longer term, this is about whether a reinforcing loop can form: DEX and AMM provide trading liquidity, a lending protocol increases capital efficiency, and institutional payment demand layers on top. This is the concrete execution path for Plan A. If DeFi primitives fail to gain traction, liquidity remains externally dependent and organic deepening stalls — which maps directly to Plan B.

8. How should XRP be evaluated right now?

The single largest analytical error around XRP today is the insistence on binary framing. "Bank coin or not?" "Public asset or not?" "Ripple's asset or XRPL's asset?" These questions are intuitive but reveal only half the picture. The more productive question is: when institutional demand attempts to enter, can XRPL's internal public liquidity structure absorb it adequately?

Through this lens, Mekras's identity challenge is not just ideological debate — it is a request to evaluate XRP within XRPL as open market infrastructure, not solely within Ripple's business frame. The SBI–DSRV research demonstrates that institutional payment narratives remain live. Schwartz's explanation reframes price from speculative target to payment efficiency variable. And XRPL's official documentation confirms that the DEX and AMM are not theoretical concepts but operational structures. The four pieces converge on a single statement: XRP's future depends not on the number of bank contracts but on how well real demand and market depth combine.

Three checkpoints for evaluating XRP's structural readiness going forward: first, native DEX liquidity depth — are DEX and AMM pools deepening to levels that can absorb institutional-scale payments without significant slippage? Currently, pool count is high at 28,000, but individual pool capital depth remains insufficient. Second, institutional payment pipeline stage — are projects like SBI-DSRV progressing from research to pilot or commercial experimentation? Currently at research stage. Third, DeFi primitive expansion — are protocols like XLS-66D being activated and drawing new capital into DEX liquidity? Currently in validator voting. If all three advance simultaneously, XRP stands to be re-evaluated as a far broader asset than "bank coin" implies. If liquidity depth fails to materialize, even strong narratives and adoption expectations cannot compensate for structural weakness.

Conclusion

XRP is too narrow if defined only as a bank coin, and too incomplete if defined only as a decentralized network asset. The more accurate framing:

XRP is an asset whose full potential activates only when institutional payment demand and public liquidity markets successfully connect.

This is not hopium. It is an intensely practical conclusion. Institutional payments can survive while shallow markets undermine efficiency. Markets can thrive while absent demand limits structural expansion. Evaluating XRP properly means examining real demand, network structure, and liquidity depth before consulting price charts. The four developments analyzed here matter precisely because they represent the moment when all three variables begin entering the same sentence again.

FAQ

Q. Was XRP originally designed as a bank asset? Per XRPL's official documentation, XRP is the native asset of the XRP Ledger, created in 2012 for payments. XRPL is an open-source, permissionless, decentralized blockchain. "For payments" is accurate, but "exclusively for banks from inception" is not a supportable characterization.

Q. Is the 'bank coin' framing completely wrong? Not entirely. Ripple's business strategy has been institution- and cross-border-payment-centric for years, so the association has a real basis. But applying that frame exclusively causes the XRPL's public market structure to be overlooked.

Q. Does the SBI–DSRV research confirm major adoption? Not yet. What has been disclosed is early-stage research exploring XRPL's viability for the Japan–Korea remittance corridor. It does, however, confirm that institutional payment use cases remain under active, realistic examination.

Q. Is David Schwartz's statement a price prediction? It is closer to a payment efficiency argument. When the same dollar amount is transferred, a higher XRP price requires fewer tokens, which can reduce market impact during large-scale transactions.

Q. Why do DEX and AMM liquidity matter this much? Because both institutional payments and public market activity ultimately require deep liquidity. XRPL's official documentation confirms the DEX has operated continuously since 2012 and that AMMs are integrated to optimize exchange rate paths across the DEX.

Q. What is XLS-66D and why does it matter? It is a proposed native lending protocol for XRPL, targeting 30–180 day fixed-term on-chain loans. Currently in validator voting stage, if approved it could channel new capital into DEX liquidity. It represents the core of XRPL's trajectory toward broader DeFi primitives beyond payments and simple exchange.

Sources

Primary Sources

| # | Source | URL |

|---|---|---|

| 1 | XRPL Docs — XRP Overview / XRPL Introduction | https://xrpl.org/docs/introduction |

| 2 | XRPL Docs — Decentralized Exchange | https://xrpl.org/docs/concepts/tokens/decentralized-exchange |

| 3 | XRPL Docs — Automated Market Makers | https://xrpl.org/docs/concepts/tokens/decentralized-exchange/automated-market-makers |

| 4 | David Schwartz original statement (X) | https://x.com/i/status/2039675984702742640 |

| 5 | Pano Mekras original statement (X) | https://x.com/panosmek/status/2039393151463383352 |

| 6 | Yoshitaka Kitao original statement (X) | https://x.com/yoshitaka_kitao/status/2039628150489964771 |

| 7 | Vet (validator) original statement (X) | https://x.com/i/status/2039858923008585940 |

| 8 | XRPL Blog — XLS-66D Lending Protocol | https://xrpl.org/blog |

Secondary Sources

| # | Source | URL |

|---|---|---|

| 9 | The Crypto Basic — XRP Should Return to Its Original Vision | https://thecryptobasic.com/2026/04/03/xrp-should-return-to-its-original-vision-not-serve-as-a-banking-tool-for-institutions-crypto-ceo/ |

| 10 | The Crypto Basic — SBI Holdings Advances XRPL Research | https://thecryptobasic.com/2026/04/03/sbi-holdings-advances-xrp-ledger-research-for-japan-korea-remittance-corridor/ |

| 11 | The Crypto Basic — Schwartz "XRP Can't be Dirt Cheap" | https://thecryptobasic.com/2026/04/03/david-schwartz-says-his-xrp-cant-be-dirt-cheap-comment-came-from-a-payment-pov/ |

| 12 | The Crypto Basic — Game Over Once DEX Gets Deep Liquidity | https://thecryptobasic.com/2026/04/03/its-game-over-once-xrp-bootstraps-native-dex-with-deep-liquidity-validator/ |

Contextual References

| # | Source | URL |

|---|---|---|

| 13 | The Crypto Basic — Daily XRP Payments Approach 3M | https://thecryptobasic.com/2026/03/14/daily-xrp-payments-approach-3m-despite-price-struggles/ |

| 14 | The Crypto Basic — 15% of Global Tokenized Commodities on XRP | https://thecryptobasic.com/2026/03/12/over-15-of-global-tokenized-commodities-on-chain-exist-on-xrp/ |

| 15 | David Schwartz 2019 PayPal tweet | https://twitter.com/JoelKatz/status/1194976049542488065 |

This content is provided for informational purposes only and does not constitute investment advice. Cryptocurrency investments carry high volatility and the risk of principal loss. All investment decisions should be made based on your own judgment and at your own risk. Independent financial advice should be sought before making any investment. Opinions, analyses, and projections contained herein reflect conditions at the time of writing and may change with market circumstances.

![[마켓 분석] 비트코인 8만 달러 앞에서 멈춘 시장](https://storage.ghost.io/c/8c/af/8caf2296-06bf-4501-ae99-5e72cb676b76/content/images/size/w600/2026/04/63d9df35-5d28-48fe-9a7a-3f651c82aafe.png)